Fifty

The Federal Reserve is widely expected to reduce its policy rate on Wednesday. Still, there’s a debate over whether the first cut will be the standard 25 basis points or a larger 50 basis points. A quarter percentage point difference in rates may not be a game changer for the economy. However, choosing 25 versus 50 would signal a somewhat different approach to the easing cycle, and that might matter a lot.

Under the best circumstances, we now face two years of Fed decisions about whether and how much to reduce the federal funds rate. Normalizing the funds rate will be tricky when the neutral rate is unknown, the data are noisy, and historical relationships remain less relevant. We are looking for principles that the Fed might apply and actions convey principles. A 25, regardless of the so-called forward guidance about future cuts, would convey more cautious easing and a greater weight on inflation risks than employment risks. Conversely, a 50 cut at the start would convey more forceful easing and greater weight on employment risks.

Since the Fed ramped up communication policy under Bernanke, it is unusual for markets to be so uncertain about the vote's outcome within days of the meeting. The market odds have been shifting around. Normally, Fed officials, especially the Chair, telegraph the decision with a high likelihood ahead of time. Powell was clear in his Jackson Hole speech last month that the Fed would cut, but he was vague on how much. My read of Waller and Williams after the last employment report was a 25 basis point cut, but the chatter did not settle down after the Fed went into its communication blackout. Plus, Powell's comments could be read as favoring 50 or at least wanting it to be seriously considered. In today’s post, I give it serious consideration.

A case for 50.

My case for a 50 basis point cut consists of two parts: one related to inflation and the other to employment. It’s a data-driven argument that does not rely on the risks of a recession, though risk management arguments for 50 basis points are compelling, too.

My interview on Yahoo Finance this morning offers the summary:

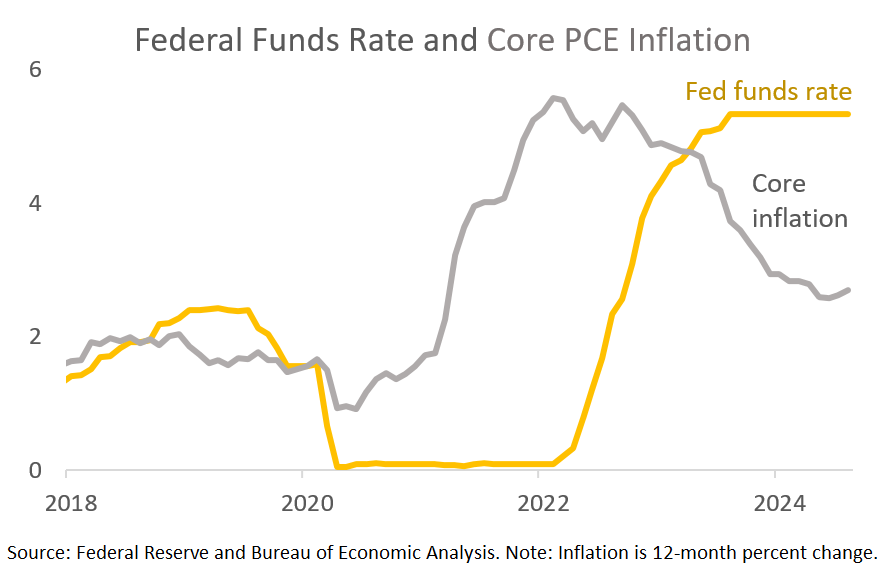

Part 1: Inflation has moved back close to the target, and the funds rate remains elevated.

Progress on inflation alone justifies the start of the Fed’s easing cycle and gets us the first 25 basis points. Fed officials have been waiting for sufficient data to be confident that inflation was moving sustainably to 2%. Since the July FOMC meeting, they have received two more months that add to inflation data at or below target (green bars). The increase in inflation early this year looks like the outlier now among several months of lower inflation since last summer. More good inflation data are key to the Fed having confidence in the sustainability of inflation’s progress toward 2%.

For August, year-over-year core PCE inflation is tracking at 2.7%, and while that’s still elevated, it’s half the peak in 2022. At the same time, the funds rate remains at its peak of 5.3%, more than three times its pre-pandemic level. The degree of restriction from the rates has not adjusted with the degree of disinflation.

While conveying some risks, the inflation data suggest that the Fed should begin cutting rates. Even if the labor market had held strong, the progress on inflation would have made the case for moving the funds rate down by 25 basis points to 5.1%.

Part 2: Labor market conditions are cooling faster than expected.

The labor market has not held strong. (See also my earlier post.) The disappointing labor market data since the July FOMC meeting should add another 25 basis points to the cut. My argument is one of recalibration and does not rest on the risk of a recession, though that could be an alternate path to 50.

The seven weeks between the July and September FOMC meetings offered more information than usual about the labor market, including two employment reports and a preliminary estimate of the annual payroll revision. The updates were decidedly more downbeat.

At the last FOMC meeting on July 31 (left panel), the three-month average of payroll gains through June was 177,000, which aligns with the 2018-19 average. The trend of gradual slowing fit Powell’s description at the time, “ Overall, a broad set of indicators suggests that conditions in the labor market have returned to about where they stood on the eve of the pandemic—strong, but not overheated. ” Only a few days later, the July employment report showed weaker payrolls, including downward revisions and another increase in the unemployment rate. The August employment report a few weeks ago was not as soft as July, but the three-month average payrolls through August now stand at 116,000 (right panel). That’s a notable shift and now below the pre-pandemic pace.

The Bureau of Labor Statistics also issued its preliminary estimate of the annual payroll revision last month. While the final estimate won’t be included in the official data until February, the preliminary estimate of -818,000 to the level of payroll employment in March 2023 would be the largest downward revision since 2009. A downward revision was expected among forecasters, but the magnitude was likely more than the Fed expected. Including those revisions (in the right panel from April 2023 to March 2024) calls into question how resilient the labor market has been during the past year in the face of a peak federal funds rate and reinforces the cooling in the July and August employment reports.

The Fed touts its “data dependence,” and this shift in the employment data, including the revisions, would be a rather large one to go without a response, especially when the funds rate is so elevated. The data suggest that the funds rate has pushed the labor market away from maximum employment, even as disinflation was underway. Adding 25 to the cut on Wednesday based on the labor market data would help recalibrate the restrictiveness.

Most arguments favoring a 50 basis point cut cite the risk of further cooling in labor market conditions, including the possibility of a recession. I agree that further cooling is likely with the hiring rate at its current, lower level. Regardless of the Fed rate cut this week, unemployment will likely increase in the coming months. It would be better to move proactively on the labor market than to wait for a negative payroll print or another jump in unemployment. The best way for the Fed to commit to its dual mandate is to respond to data since the July FOMC meeting that shows a cooling in the labor market.

25 is not good enough.

Various arguments exist for a 25 basis point cut, but they generally miss some important context or misunderstand the Fed’s mandate. Here are three hypothetical examples (in italics) in favor of 25 basis points with my rebuttal, conceding that there are risks around any action:

When the Fed cuts, it cuts by 25 basis points unless we are in a crisis. We are not in a crisis, so there’s no reason to cut by 50.

By this point, we should all be skeptical of arguments in this cycle that rest on history alone. The global pandemic and the resulting shifts in behavior and policy caused a series of highly unusual, wide-reaching economic disruptions. The past can provide insights but should not be the deciding vote. Comparisons of the current inflation to the 1970s were incomplete, and as a result, the advice that a recession would be necessary to bring inflation down was deeply flawed. Arguments about the appropriate size of a cut now should be grounded in arguments about the current environment. The right size for a cut depends in part on the funds rate level. The Fed chose to hold off the easing cycle, which also stands out in historical comparison. After that delay, a larger rate cut would help normalize the funds rate more quickly.

Aggregate demand measures (in GDP or high-frequency data) continue to expand at a solid pace, so the Fed does not need to cut, and a large cut would risk more inflation.

It’s important to note that the Fed has a dual mandate of stable prices and maximum employment. It does not have a growth mandate or growth target. Moreover, solid growth does not always signal an overheating economy. The notable disinflation in the second half of last year was accompanied by over 3% GDP growth. Improvements in supply, like an increase in the labor force and higher productivity, can boost growth without sparking inflation. It is true that a larger rate cut likely comes with more inflation risk. However, with slack in the labor market, a pickup in demand should not be a problem in terms of inflation and would be beneficial to avoid further cooling in the labor market. The Fed “needs” to act when its dual mandate is under threat.

The Fed can start small with its first cut and signal that it will do larger cuts if labor market conditions deteriorate or a recession occurs.

Words or dots (in the Summary of Economic Projections) alone won’t be credible now. The Fed embraced “forward guidance” after the Great Financial Crisis of 2008, when the funds rate was at the zero lower bound. The Bernanke Fed signaled via the Summary of Economic Projections, press conferences, and speeches that it intended to keep rates low for a long period of time to push down market rates even though the Fed could not lower the funds rate more. But it’s 2024 and the Fed is no longer constrained with the fed funds rate north of 5%. A 25 basis point cut will raise questions about the Fed’s willingness to react to further weakening, regardless of how dovish Powell is at the press conference or how many cuts are in the dot plot. In addition, it takes time for interest rates to work through the economy. If the Fed waits until the economy is in a recession to make large cuts, it has waited too long to avert the recession or even soften its blow.

Anything more than a 25 basis point cut from the Fed would signal panic to markets.

The Fed should choose the right policy and then worry about communicating it well. There are many ways to maintain calm. A 50 basis point cut with some dissents and projections with more modest cuts would reinforce that the Fed is reacting to data, not flipping to a sequence of large cuts as it might in a crisis. Getting ahead of potential risks before they become a crisis can instill confidence. The communication on Wednesday will be important, and Powell is a good communicator. What’s most important is the policy.

In closing.

I expect a 50-basis-point cut on Wednesday.

The Powell Fed takes both sides of the dual mandate seriously. It also takes the data seriously and is willing to recalibrate when the data surprises. We saw that in the tightening cycle and before the pandemic.

Seven weeks ago, the Fed was on track for a 25-basis-point cut, but since then, with disappointing data on labor market conditions, that is no longer sufficient. A vote for 50 this week is a vote for the dual mandate and a vote for data dependence. That’s a good commitment to reinforce as the Fed starts the last phase of the soft landing: getting out of the way.

Thanks for another clear and informative letter. (Also, the latent grammarian in me repects the use of the plural verb-form with "data.")

50 basis points. You nailed that with your explanation and prediction. I’m not surprised. Congratulations.