Who's afraid of a negative payroll print?

Jobs Day will likely be messier than usual with recent hurricanes and a strike weighing temporarily on payrolls. Even with solid underlying growth the headline could look rough.

Today’s post previews Friday’s Jobs Day and explains why the headlines might be misleading. Specifically, temporary factors may weigh down the payroll estimates in addition to the usual noise in the data.

Lots of noise in payrolls.

Fed Governor Chris Waller recently shared his view on the distortions to October:

I will be looking for more evidence to support this outlook in the weeks and months to come. But, unfortunately, it won't be easy to interpret the October jobs report to be released just before the next FOMC meeting. This report will most likely show a significant but temporary loss of jobs from the two recent hurricanes and the strike at Boeing. I expect these factors may reduce employment growth by more than 100,000 this month, and there may be a small effect on the unemployment rate, but I'm not sure it will be that visible. Since the jobs report will come during the usual blackout period for policymakers commenting on the economy, you won't have any of us trying to put this low reading into perspective, though I hope others will.

That’s a substantial distortion that could mask what would otherwise be a ‘good news’ report and make it look decidedly ‘bad news.’ Moreover, seeing an October set up for our first negative payroll estimate in a while is not hard.

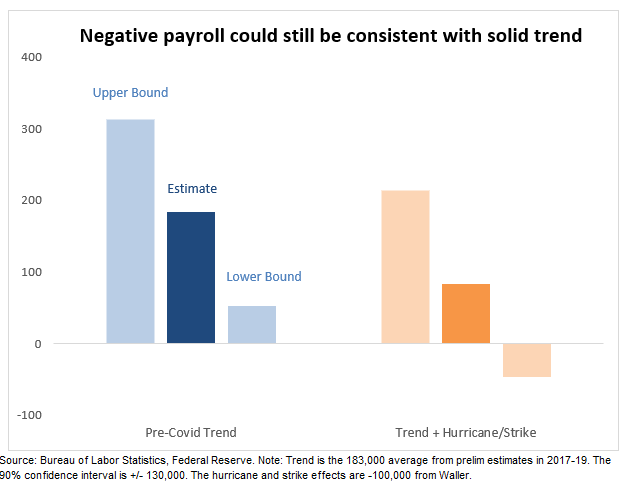

Let’s start by assuming that the underlying pace of payroll gains is back to its 2017-19 average of 183,000 per month. (The dark blue bar on the left below). Setting aside the hurricanes and Boeing strike, the initial estimates are always imprecise. (See my earlier post on statistical confidence.) The 90% confidence interval based on survey sampling error is +/- 130,000. (The light blue bars.) So, even if payrolls were on trend, the estimate range could be large.

The orange bars to the right subtract 100,000 off the trend for Hurricanes Helene and Milton and the Boeing strike. When the confidence interval is added, the 90% lower bound is almost -50,000. A negative print would ruffle some feathers, but at least in this example, it could be consistent with a solidly growing labor market.

Noise, especially in initial monthly prints, is nothing new. In the three years before the pandemic, about 10% of the months had prints below 100,000, and one in September 2017 had a negative print. Note that was the same month as Hurricanes Harvey and Irma.

Negative payroll prints are not uncommon, even in good economic times. The October 2024 print is a good candidate for one, given the extra factors from the hurricanes and the strike. A low print alone does not mean the labor market is slipping. Other parts of the release and outside data will help unpack the headline.

Keep an eye on the unemployment rate.

The employment report will be messy, but that does not mean we can’t learn anything. For example, a move in the unemployment rate—consensus is flat at 4.1%—would be less likely due to distortions from the hurricanes or the Boeing strike than payrolls would be. A softening in labor market conditions is possible, given that the hiring rate remains well below its pre-COVID average.

As I explained before, the low hiring rate is likely putting upward pressure on unemployment. So, a notable increase in unemployment in October would be a setback in the stabilization narrative.

Note that the Sahm rule will turn off—falling below the 0.50 threshold—if the unemployment rate holds steady at 4.1%. It will also turn off if the rate rises by only one-tenth percentage point since the low in the 12-month look-back window is rising. The Sahm rule turning off would mark the first episode since the late 1960s for it to trigger on and off without a recession. It does not say anything about the chances of a future recession but underscores how unusual this period has been.

In closing.

All eyes remain on the labor market, but October will likely be tough to watch. More than ever, we must read through the details carefully.

Beware of the scary headlines.

Great to know you feel good enough to cogently write up this great perspective!! Keep going!

As I said before my concern is landing softly but in sticky mud. The corresponding comfort is that the foundation of the US economy is strong enough to handle that as well and to remain “the envy of the world” for the next three months, or until the effects of the results of elections, both here and overseas, start showing up.

We won't get a Negative Payroll Print until the New More Honest Regime takes over.....

The BLS has become a Politically run agency....

How did these geniuses at the BLS have a 30% error in their calculations ??

Because those calculations were Intentionally High, in order to prop up the current Leftist Regime.