We need to restore balance: a recession is not the path to balance

For over a year, the Fed has barked at us that the labor market is "out of balance." There's more to the story. We do lack balance across the entire economy. It's time to get real about how to fix it.

At the last press conference of 2022, Fed Chair Jay Powell said it again:

Although job vacancies have moved below their highs and the pace of job gains has slowed from earlier in the year, the labor market continues to be out of balance, with demand substantially exceeding the supply of available workers. The labor force participation rate is little changed since the beginning of the year. FOMC participants expect supply and demand conditions in the labor market to come into better balance over time, easing upward pressures on wages and prices.

In a new twist, after two months of encouraging news on inflation, the Fed is now telling us they are focused on inflation in the non-housing services, which is still too high. And it’s an area that the Fed claims are especially sensitive to wage growth. Assumptions stacked on top of assumptions. The ‘War on Workers’ marches on.

Why isn’t the Fed asking why we are living with a labor shortage? Why isn’t it asking about the benefits of wages with some bargaining power? Why isn’t it asking about the other imbalances causing this strange labor market? Why?

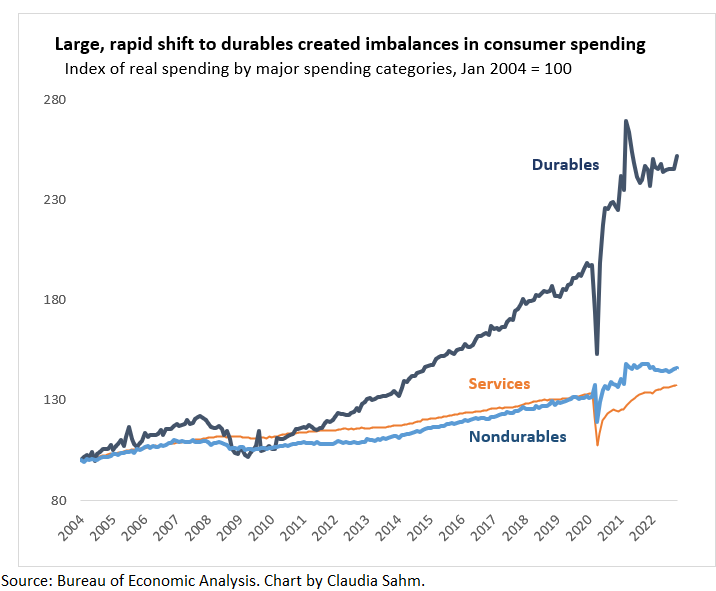

Consumer spending is out of balance.

Nearly 70% of GDP is consumer spending. What consumers buy and are willing to pay is the primary driver of inflation. As Matthew Klein has argued in his excellent The Overshoot Substack, wage growth affects inflation via its effect on income. Wage compensation is the primary source of income for most Americans. More income, especially for those families living paycheck to paycheck, means more spending.

I am adamant that bigger paychecks are a good thing; the well-being that comes from spending (and netting out the pain of working) is the goal of every economic model. Shockingly, many of my macroeconomist peers think the goal is low inflation. Please show me that model. Good luck; it does not exist.

So what did consumers do when they got stimulus checks and bigger paychecks during the pandemic? They bought stuff. Less on experiences (services) and more on goods, especially durable. It was a huge and rapid swing.

I worked for over a decade as one of the leads on consumer spending at the Fed, starting right before the Great Recession began. I am shocked that this swing was so large and so persistent. It is an unprecedented and major imbalance.

Three years later, we have only started to see balance beginning, but we have miles to go. And the swing back to normal will be a big deal with ripple effects throughout the economy. Durable goods, by definition, have a useable lifespan of years; those washing machines and desks bought during the pandemic will not need to be replaced for some time. Spending is flow, something we do at every point in time. It does not always grow, especially in areas like durables, where it is prone to fall. Downward pressure on inflation from goods is only starting.

Don’t believe me? Ask the chip producers who are seeing their inventories build.

It sure helped me out too. I got holiday deals, like a $200 ThinkPad for my parents, which I spent several hours setting up, transferring, and organizing all the files from their decade-old iMac. That ThinkPad sale—normally lists at $900—should be in CPI.

Back to the massive imbalance in our types of spending: without a doubt, the trillions of dollars in relief from the CARES Act through the Rescue Plan contributed. And yet, the pandemic, with the initial shutdowns, switch to work from home (my dishwasher broke from a lot of extra use), multiple waves of the virus (going out to dinner was not safe), incomplete vaccinations, and ongoing health risks of death and disabilities (we bought an air purifier), also upended the pre-Covid balance in the mix of spending.

Such a spending imbalance would have put immense burdens on supply chains and goods production, regardless of whether consumers had had an extra infusion of cash or a raise. Rich people, who didn’t get a dime of stimulus checks, spent a lot of money on their ‘creature comforts’ at home and furnishing their second homes.

As with the unclogging of supply chains, the return to the pre-Covid trend in demand for goods and services is slow and far from complete. Plus, did you think hiring them back would be easy after laying off millions of service workers within weeks at the start of the pandemic and botching the Payroll Protection Plan? Want to blame someone, blame the CEO and shareholders of the hotel chains, upscale restaurants, and temp agencies that contract our cleaning staff.

I was outraged listening to this Odd Lots episode. Cry me a river, buddy, that you have had a hard time rehiring after you laid off your whole service staff within weeks. How did you think that would build your ‘brand loyalty"‘ as an employer?

But the blame game can wait. What is urgent is for the Fed to stop and be patient. The next meeting should be an even smaller increase in the federal funds rate or none at all. More relief on inflation is coming here. Wake up, Fed.

Where workers are working is out of balance.

Not surprisingly, the massive imbalances in consumer demand led to imbalances in the mix of jobs. Again, millions of service workers were laid off, and delivery and manufacturing businesses were desperate for workers. Guess who pays more, even before the pandemic. Contrary to the trope, the unemployed do not like being unemployed. Only a portion of them could get enhanced unemployment benefits, and many derive a sense of purpose from working.

About that pay. Here’s one of many examples:

Average hourly pay at an Amazon warehouse: $17 per hour.

Average hourly pay at Mc Donalds: $11 per hour.

That’s almost 50% more. Both of these jobs are brutal. Turnover among low-wage jobs is over 100% per year. Amazon publicly touts t its business model as workers stay only a year. I have a friend from high school who had open heart surgery last year and then took a job at a nearby Amazon warehouse. The pay was much better than her desk job at an auto repair shop, but Amazon is much more physically demanding. The U.S. economy relies on an endless supply of low-wage workers with no bargaining power. It’s a pick-your-poison reality for most workers.

It would be super if the rich and powerful stopped ‘poisoning’ workers. We are in this together. You need them as much as they need you. But that’s going to take a long time to sink in. Currently, the higher-paying but brutal jobs in goods are ‘winning.’

I was home on the farm in Greenfield, Indiana, for Christmas. My youngest brother, who now sells construction and farm equipment, took me on a driving tour past the numerous new warehouses nearby. We are right next to I-70, a major East-West trucking route. The warehouses are huge. The unopened Walmart one is even larger than the massive Amazon one. Another was built by someone speculating that the demand for warehouses was endless. He should have looked at the consumer demand imbalance. Nobody’s bought that warehouse. I bet he’ll be waiting a while.

Another fascinating and welcome ‘imbalance’ in the labor market is the stronger return of full-time relative (left) to part-time jobs (right). It’s obvious that benefits like health insurance and the reliability of set hours are good things. It’s also obvious that a job-full recovery like this time is much better than a jobless one like last time.

The Fed is out of balance.

The fact that the Fed has lost its balance is apparent to anyone who pays the slightest bit of attention to them. Most people don’t. I do.

I have a post for paid subscribers later this week on how that imbalance shows up in the Summary of Economic Projections. In addition, I will give you the ‘cheat sheet’ on the signs that the Fed is close to stopping; it’s not the CPI and Average Hourly Earnings; it’s their interpretation. And they ain’t even close now. For better or worse, the SEP is the best read we get on their thinking. I will put on my Fed decoder ring and draw on over a decade inside the house to unpack. So subscribe. It’ll be worth more than $10 (my monthly paid subscription).

In closing.

I am a vocal and colorful critic of Fed policy. I am increasingly frustrated with its actions and words. Actions matter most, and words are important too.

The Fed must hire a real person. Here’s an idea: hire one of the contract workers in the cafeteria full-time and have them Jay. Rather than being hell-bent on smaller raises for workers and your credibility, listen to the people your policies affect. Ya ain’t losing your job. Your paychecks at the Board aren’t too shabby now. And I promise you will make a shit ton [technical macro term] of money after you finish with Wall Street jobs and in speaking fees.

Let’s make 2023 the year we move back toward balance. That’s my hope. Here’s my contribution to Peter Coy’s newsletter at The New York Times:

All year people from Larry Summers, a former Treasury secretary, to Cardi B., a rap icon, told us we are either in a recession or headed toward one. I disagree; jobs are plentiful, and the unemployment rate is near its 50-year low. The reason we fear recessions is because millions of workers lose their jobs. In fact, historically, even a relatively small rise in unemployment tells us we are already in a recession and substantially more unemployment is on the way.

My widely followed Sahm rule formalizes that dynamic. [See my post last week on it.] It says that if the unemployment rate rises by 0.5 percentage point or more, we are in the early months of a recession. My hope for 2023 is that the Sahm rule “breaks” for the first time. What would that mean? Unemployment increases by 0.5 percentage point or more from its 2022 low — which is near certain, given the Fed’s aggressive interest rate hikes — but doesn’t go much higher than that. Unlike in the past, inflation could come down without high unemployment and a recession.

Even better would be for us to move toward a balance that’s even better for workers and families than before the pandemic. We can and we must. Finally, read Coy’s entire piece. Unsurprisingly, the best ones come from real people. Listen to the people.

Love it! From what I understand, real wage growth has been stagnant for decades. Wage growth would give workers the chance for the American dream now, versus putting some away each month and hoping that investments "might" pay for an easier, RV filled life later. I don't know how you restore wages and worker bargaining power and avoid the upward spiral of inflation that you have spoken of previously, except by mutually agreed upon trust between manufacturer and worker.

It’s surprising there’s been so little talk about how tax policy over the past 30 years has evolved to disincentivize work. When people can make a living from investing in Airbnbs or tiktoking or living the capital gains passive income dream, why bother with a job that actually produces stuff? If we’re serious about policy incentives to work and expanding labor supply, we need to equalize the tax gap between labor and capital income. Right now, you’re a fool to rely on labor income if you have the asset wealth to avoid it.