The Sahm rule: I created a monster

The Sahm rule is a widely followed indicator of recessions. It's gotten a lot of attention from experts who use it to argue we're not in recession and others who weaponize it to say one is coming.

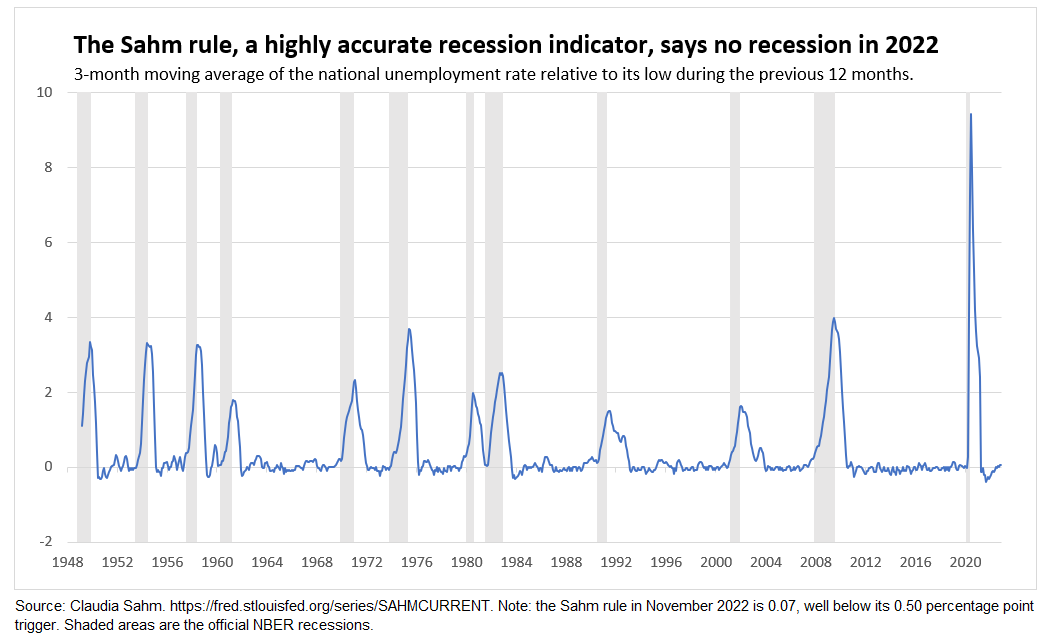

The Sahm rule is simple:

When the three-month moving average of the national unemployment rate is 0.5 percentage point or more above its low over the prior twelve months, we are in the early months of recession.

Get relief to families fast in recessions.

The Sahm rule was born for a specific purpose: a tool for better policy.

I created the Sahm rule to send out stimulus checks automatically. The idea was to act fast to make the recession less severe and help families. The star was always the stimulus check, not the indicator that other people named after me. See my proposal in the Recession Ready: Fiscal Policies to Stabilize the American Economy, published in early 2019. I left the Fed to work with Congress on new automatic stabilizers. I did. The Sahm rule was the trigger for the proposals in Congress. Then came Covid.

I never dreamed the Sahm rule would turn me into a recession expert. It has.

Historically, after the Sahm rule was triggered, unemployment kept climbing. Even in the mildest of recessions, like 2001, unemployment rose two percentage points from its pre-recession low. That would predict an increase in the unemployment rate from 3.5 percent in 2022 to at least 5.5 percent in 2023 or 2024.

The Covid recession is a massive outlier. The unemployment rate shot up at lightning speed when the economy shut down and started falling rapidly within months.

Recessions are always bad. Millions of workers lose their jobs. And millions more lose job opportunities and bigger paychecks. Crushingly, it hurts those with the least the most. None of the experts emphatic that we “need” a recession will lose their jobs. No Fed official hiking interest rates aggressively will either.

The Sahm rule as a weapon.

I created a monster.

I took ten days off from work over Christmas. No press. No following the macroeconomic debates, including ones that quote me and the Sahm rule. And then my peace and quiet was invaded.

Larry Summers wrote a Washington Post opinion piece in which he mentioned the Sahm rule. Multiple people sent it to me. One mentor and friend emailed me, “Dear Claudia, Congratulations! You have Larry Summers citing the Sahm rule here.” Here’s him on the Sahm rule:

Unfortunately, all major reductions in inflation in the past 70 years have been associated with recessions. It should come as no surprise that many economists, including me [not me], expect a recession to begin in 2023. Historical experience as encapsulated in the proposition known as the Sahm Rule demonstrates that whenever U.S. unemployment rises by more than half a percent within a year, it goes on to rise by 2 percent. So, if recession comes it is very likely to lift unemployment to the 6 percent range.

Repeat after me: the Sahm rule is an empirical regularity. It’s not a proposition; it’s not a law of nature. See my post from earlier this year:

If the Sahm rule is ever gonna break, it’s next year.

I created the Sahm rule, and I take full responsibility for it. And I am the expert on it. So when I say it could break, you should take my argument seriously.

What does mean to “break?” The unemployment rises 0.5 percentage point and then stops around 4 percent, that’s unlikely to be called a recession. And that’s never happened. Normally, once the unemployment rate gets going it goes a lot. So the Sahm rule triggering and no recession, that ‘breaks’ the rule’s stellar record.

Here’s me in an excellent piece from Jeanna Smialek last week in the New York Times :

Typically, when the unemployment rate rises by more than 0.5 percentage points, like the Fed forecasts it will do next year, the jobless rate keeps rising. Loss of economic momentum feeds on itself, and the nation plunges into a recession. That pattern is so established it has a name: the Sahm Rule, for the economist Claudia Sahm.

Yet Ms. Sahm herself said that if the axiom were to break down, this wacky economic moment would be the time. Consumers are sitting on unusual savings piles that could help sustain middle-class spending even through some job losses, preventing a downward spiral.

“The thing that has never happened would have to happen,” she said. “But hey, things that have never happened have been happening left and right.”

What’s a thing that happened for the first time this year? Two consecutive quarters of declining GDP, not in a recession. A two-quarter decline has occurred thirteen times since World War II, each time in an officially dated recession, except in 2022.

There is no way the NBER’s Recession Dating Committee will say we were in a recession in 2022.

GDP, a highly reliable indicator of a recession, broke. Why stop now?

Sadly, of course, the Sahm rule might not break. We could have a recession next year. That’s my fear for the American economy. Even in the best case, I expect the Sahm rule to trigger sometime in the middle of next year, with the unemployment rate rising to 4 percent.

In every recession except the Covid recession, unemployment rose slowly. Typically it’s a year from low to high. So, we likely won’t know whether unemployment has stopped rising and whether a recession will be avoided until the end of 2023 or even 2024.

In closing.

The pandemic has disrupted our lives and livelihoods in unimaginably awful ways. Then came a horrific war in Europe with food and energy supply disruptions. After three years of rolling crises, the “unprecedented” are piling up and are mostly bad. I want one more unprecedented, a good one. The Sahm rule breaks: unemployment rises less than ever after it triggers, inflation comes down, and we avoid a recession.

That’s the path back to some semblance of normal. By this time next year, but not much sooner, we should know if we are well on our way there. I’m cautiously optimistic. And I am exhausted and nearly broken from all the bad events, so I won’t make promises that I can’t keep. Even so, there are glimmers of light.

Hope is not a policy strategy. Hopelessness is not either.

Source: Getty Images.

BRAVA! YOU GO GRRL!

Thank you for clear vision in murky times.