It's the pandemic, stupid

Fed week. Everyone will be listening for clues on how the Fed might react to three months of disappointing inflation. It's what we won't hear that matters.

Programming note: If you would also like to read shorter notes from me on macroeconomic conditions and the Federal Reserve, follow New Century Advisors on LinkedIn. We will be posting there regularly. I will continue to write here and on Bloomberg. I have lots to say!

For almost three years, inflation has been higher than before the pandemic. We have made considerable progress in it coming down, especially in the second half of last year. However, the first three months of this year were rough. The inflation story gets complicated quickly when we look under the hood. Nothing ever fully explains something complicated. This time is no different, but Covid and the economic disruptions it caused loom large in this inflation cycle.

That’s been a refrain from some, including myself, as soon as inflation took off. (My post in 2021.) What I got wrong was how profound the disruptions would be and how slowly they would unwind. Getting that wrong, especially the timing, meant some economic policies were wrong—sometimes too much and sometimes not enough. That’s a critical discussion, but for another day. Today is Covid.

Covid echoes in inflation.

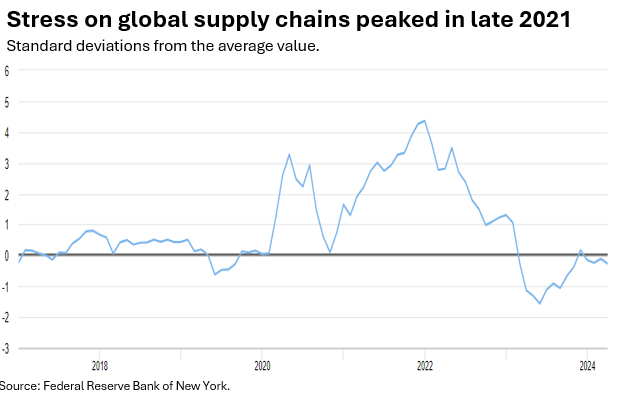

The motor vehicle sector is the ‘poster child’ for the economic disruptions caused by the pandemic. Global supply chains broke down early in the pandemic.

That made it nearly impossible for auto producers to make enough new vehicles to meet demand, so prices increased rapidly. Then, would-be buyers moved to the used car market. The flood of demand—which fiscal relief and low interest rates also boosted—massively increased used car prices. As supply chains were unclogged, motor vehicle inflation began to fall in early 2022.

So, that was it? No. The broken supply chains pushed up the prices of vehicle parts (dashed blue line) at the same time as motor vehicles. That inflation has fallen back since mid-2022 and is, along with vehicle inflation, back to its pre-pandemic pace.

With the rising prices of motor vehicles and parts and labor shortages, high inflation spread to motor vehicle services. Inflation in vehicle repair and maintenance (orange line) rose in mid-2022 and has fallen since mid-2023, albeit with a recent uptick. Finally, the surge in motor vehicle insurance prices (yellow line)—which reflects higher vehicle and maintenance prices, lost profits due to the inability to adjust contracts quickly when other prices rose, and some non-Covid factors—is ongoing. Motor vehicle insurance premiums continue to rise at a fast clip and are currently a large contributor to CPI inflation.

Motor vehicle services have been one of the stickiest parts of ‘supercore,’ services excluding energy services and shelter. It is also an example of the echoes of Covid disruptions. That inflation is not about excess demand now; it’s an incomplete healing. The passage of time, not higher interest rates, will solve the problem.

The rapid shift in spending behavior has unwound slowly.

We must be cautious with stories about Covid disruptions. Using specific types of spending to diagnose overall inflation can be misleading. If consumers do change their spending patterns, it can show up as a boost to inflation, but that’s a hard diagnosis to make and doesn’t necessarily mean inflation will move back down. Owen F. Humpage at the Cleveland Fed lays out the role of relative prices:

Relative-price changes, like inflation, can cause price pressure in an economy. We experience them every day much like we experience inflation, and they cause changes in standard price indexes. But there the similarity ends. Relative-price changes are not a monetary phenomenon. They arise in market economies as individual prices adjust to the ebb and flow of the supply and demand for various goods. Relative-price movements convey important information about the scarcity of particular goods and services …

In this way, relative-price changes—no matter how uncomfortable they are for consumers or producers—transmit vital information necessary for the efficient allocation of resources throughout any market economy. Inflation, by contrast, contributes no information useful to our consumption, production, or labor choices. If anything, inflation can temporarily distort vital relative-price signals, leading people to make unsound economic choices.

The Arthur Burns Fed made the mistake in the 1970s of attributing too much of the high inflation to oil price shocks and other events outside the Fed’s control, causing underlying inflation to get out of control.

What’s out of control now? Parallels drawn between now and the 1970s are out of control. Back then, people had developed an ‘inflation mentality,’ that is, they began to expect higher inflation. That led them to bargain for higher wages—with prevalent unions or a general norm of cost-of-living raises. Businesses passed the higher costs on to consumers. We do not have that mentality, and we do not have a wage-price spiral. It’s not the 1970s. It’s 2024.

Covid kicked off a dramatic, albeit temporary, shift in buying patterns. Within months of the pandemic's start, goods spending as a share of total spending shot up—even before the rise in goods prices. That share only began to turn down in late 2022 and remains somewhat elevated.

I worked for over a decade at the Fed as a lead on consumer spending—doing current analysis and forecasting. No other change in the Covid economy blew me away more. It may not look like much, but it’s a massive shift in what consumers wanted and what businesses had to produce. That was disruption, and it lasted for some time.

Covid forced that shift, which was not a choice, and has slowly unwound with the pandemic. At the start of the pandemic, schools closed, most businesses went remote, and broadly, the fear of infection kept people at home even in their free time. And so the money people spent shifted rapidly to buying many more goods and much less services. It would have stressed business in good times, but it occurred at the same time that a breakdown in global supply chains made it harder for businesses to meet the sharp increase in demand.

Build, baby, build.

Let’s start with the punchline: NIMBY-ism must end. We must build more housing, any housing, in this country. Want to stay the best? Build.

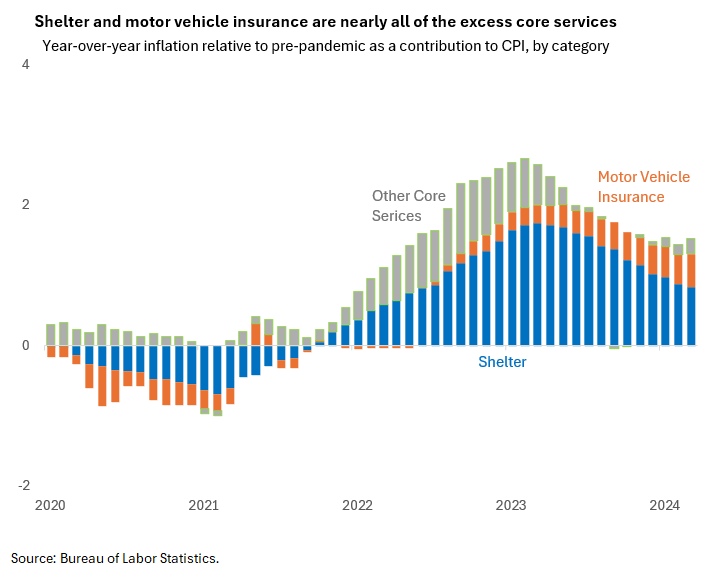

The thin silver lining of the month-after-month of high inflation readings is a loud and clear, “build, baby, build.” We must listen. The US went into the pandemic with an underbuild of housing, and Covid blew it out.

What happened? First, we had a surge in ‘household formation’ in the pandemic, that is, people moving out on their own or starting families. Low interest rates, stimulus money, the strong labor market recovery, and work-from-home boosted housing demand. However, that new demand crashed into the existing lack of housing supply. In addition, clogged supply chains and labor shortages made it hard to build more housing. The result was a surge in rental prices in 2022. The way that the cost of shelter for renters and homeowners is calculated in the CPI meant that the effects in the CPI were slow to show up and even slower to fade. The contribution of shelter to the inflation data peaked in 2023 but remains the biggest contributor to inflation.

Recently, we have heard the United States lags in its fight against inflation relative to Europe. This is not true. If we measure inflation the same way Europe does, the US (blue line) hit its pre-pandemic level of inflation in the fall of 2023. The biggest difference is the treatment of shelter inflation. The pickup in inflation this year is also muted when we compare apples to apples.

The implications are real. European central banks are likely to begin lowering rates sooner than the United States since their inflation appears to be lower than the United States. The Fed chose its target inflation rate in PCE (green), and it’s not time to change course, but it’s important to understand the global implications.

Closer to home, there are problems with US monetary policy when shelter inflation looms large. It takes time for changes in interest rates to work their way through the economy and affect overall demand. The only things that interest rates can affect are current and future demand. No level of interest rates now can go back and stifle household demand for housing two years ago. The inflation in new tenant rents—which is down markedly—is a better signal of the current demand for sheltery, but it’s not fully reflected in the CPI and PCE. The Fed is tying forward-looking monetary policy to the most backward-looking part of inflation. That’s a risky move.

Being ‘data-driven’ should not mean blindly following topline numbers. Yes, other parts of inflation are somewhat elevated, but the Fed said it will not wait until 2% to cut. Current inflation is not far, especially when you put less weight on the deeply backward-looking parts. I don’t blame the Fed. Its tools are limited, but I disagree.

Again, every person who is angry about inflation should go to their local planning board and demand more high-density housing in their neighborhood. That’s what we must have to be a vibrant economy. Housing is crucial.

In closing.

Covid is in the rearview mirror for millions of Americans; for others, it was never real, and others still struggle with direct health effects. Regardless, its imprint on the economy remains. We are well beyond the spring of 2020 but not fully back.

We can’t solve a problem that we won’t diagnose. If we don’t solve the problem this time, when it comes again, we will be left with the same approach: the passage of time. We can do better next time, but we must learn.

As a bonus, here’s my conversation last Thursday on Let’s Talk Markets, where I joined hosts Dave Lauer and Pink at Urvin Finance and co-guest Ophir Gottlieb.

I said very early this inflation was driven by shelter inflation and I agree,that higher interest rates will not be helpful in solving it.

Most of mainstream macro needs to get in their heads that high rates aren't going to fix the inflation that is driven by rent and shelter costs. Its also remarkable that they don't realize that the higher rate environment is adding to inflationary pressures. Oddly enough, the re-acceleration of inflation is gravitating towards the FFR.