What's up with wages?

Hourly wages of workers rose 0.6 percent in November. That was higher than expected and stoked fears of more inflation. Not so fast [literally] there's more to this story.

Today’s post is largely a guest post from Riccardo Trezzi, the founder of Underlying Inflation, Trezzi Consulting, and a former inflation expert at the Federal Reserve. I worked with Riccardo at the Fed and always find his thoughtful, data-driven analysis illuminating.

Last Friday, on Jobs Day, the inflation hawks fixated on the 0.6 percent jump in average hourly earnings (AHE). They argued that the unexpectedly strong increase meant the Fed’s fight against inflation would be harder and require even bigger rate hikes than expected, raising chances of recession next year higher.

I firmly disagree, as I explained in my recent piece:

But there is much more to dig into with the wage data.

Above all, is that 0.6 percent even an accurate reflection of how fast employers' wage costs are rising, costs that they might pass on to consumers? Is it a sign of bigger paychecks that will boost demand and inflation? Remember, the Fed’s one tool to fight inflation, interest rate increase, works by reducing demand. More demand due to strong wage growth could get in the way of its effort and sustain high inflation.

Here is Riccardo Trezzi on how to think more about that 0.6 number. It’s a shorter, lightly edited (for a less technical audience) version of his subscription newsletter, a must-read for anyone who wants to understand the nuts and bolts of inflation now and insights on where it’s headed.

Note, Riccardo is less optimistic than I am about inflation moving down notably next year, though we agree last week wasn’t bad news for the Fed on the inflation outlook.

What’s up with wages?

How much did the 0.6 percent monthly increase in Average Hourly Earnings (AHE) in November tell us about the labor market? That is, how much “signal” did it contain? How does it compare to other signals from other indicators of wage growth?

We [that’s Trezzi, and does not include me] analyze the recent developments in the Average Hourly Earnings (AHE) as well as other wage and total compensation measures and explain how the Fed likely interprets the latest estimate.

Main Takeaways:

The 0.6 percent increase in Average Hourly Earnings in November is probably overstating the underlying wage growth, but it remains robust.

Wage and possibly total compensation growth remains above the level consistent with the Fed’s 2% inflation target.

There are faint signs of total compensation disinflation, but overall, we remain skeptical of both wage disinflation and wage re-acceleration.

Wage disinflation will take time. We are not there, not yet.

We believe that the Fed staff largely agrees.

Far fewer businesses responded to the survey last month.

The survey response rate of (business) establishments dropped significantly in November, which may have made the estimate of wage growth less reliable.

The establishment survey’s response rates for the first estimate by month dropped more in November than in the last seven years. [Note that all the survey estimates—including payrolls—may revise next month when more establishments report.]

While the reason behind this drop is still unclear—the suspect is the timing of Thanksgiving—similar declines have been recorded in other surveys in recent months, including Job Openings and Labor Turnover Survey (JOLTS). It raises serious concerns about the quality and reliability of the estimates. The Bureau of Labor Statistics said it tested for and did not find signs of bias, up or down. But from what we know now as external experts, it is possible the data could be biased up or down.

We should interpret the current 0.6 percent wage growth estimate with great caution.

The drop in hours pushed up wage growth and may signal less, not more, demand in the economy.

Average Hourly Earnings (the hourly wages) are average weekly earnings divided by average weekly hours. Hourly wages can increase because the weekly earnings (the numerator) go up or the weekly hours (the denominator) go down.

The implications for demand and inflation are different.

From an aggregate demand perspective, one should expect higher hourly wages to lead to larger weekly paychecks, but only if wages rise more than hours fall. In that case, it could lead to more spending and inflation. That’s unlikely to happen if hours fall more than wages rise and workers get smaller paychecks.

Average weekly hours declined from 34.5 in October to 34.4 in November. See the table. If hours had not changed, then instead of wages increasing 0.55 percent, month over month (MoM), they would have risen only 0.26 percent. That’s a much smaller increase; inflation hawks would likely have ignored wages and focused on solid payrolls.

But, it’s important not to just ‘adjust’ one monthly estimate due to a decline in hours. Usually, how much do hours change? Not much, except in recessions and recoveries.

Before Covid, hours were roughly stable at around 34.5, excluding the Great Recession. However, when the pandemic began, hours increased significantly and then moved back toward pre-Covid levels.

The estimates of Average Hourly Earnings understated the boost to aggregate demand early in the pandemic and have overstated it in recent months.

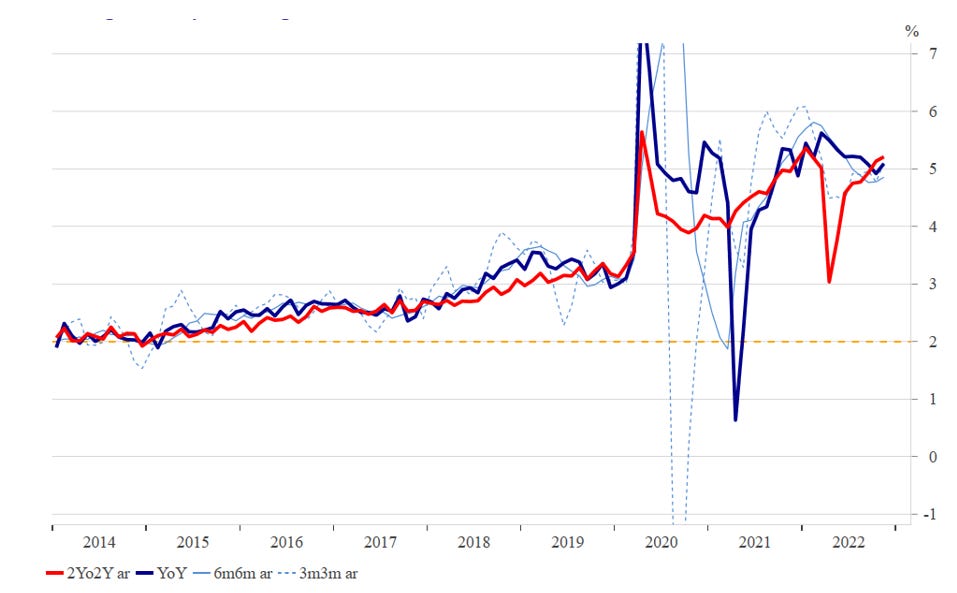

Smoothing out the month-to-month wiggles better measures the underlying level of wage growth.

An easy way not to be head faked by a monthly estimate is to average across months, such as across three months (3m/3m at an annual rate), six months (6m/6m at an annual rate), year over year (YoY), and two years (2Yo2Y at an annual rate). Currently, all these estimates are around 5 percent, which is well below the 6.6 percent at an annual rate in November relative to October and does not show a sudden pickup.

According to Average Hourly Earnings, wage growth shows no signs of slowing down or moving up. Plus, this is consistent with the Employment Cost Index (ECI) a better measure of total compensation. So, no news here. No reason to revise your inflation forecast.

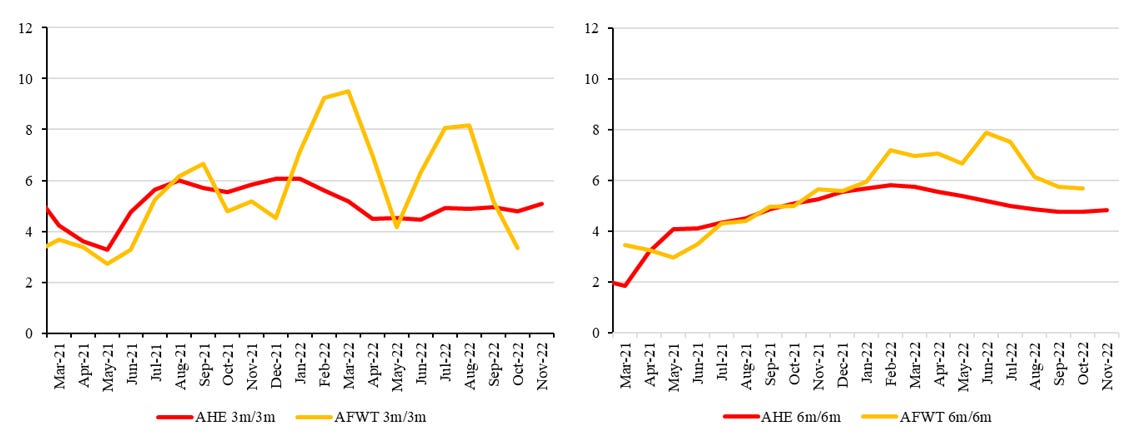

Other measures of wage growth are relatively stable too.

The Atlanta Fed Wage Tracker (AFWT) is an individual worker's wage increase. The tracker only reports the year-over-year changes, but Justin Bloesch, a post-doc at Columbia, calculated the three-month and six-month changes.

Wage growth in the tracker has also leveled out, seen in the year-over-year (YoY) moving sideways. The three-month change is lower than the six-month, 3.4 percent and 5.7 percent, respectively. The pattern is similar to Average Hourly Earnings.

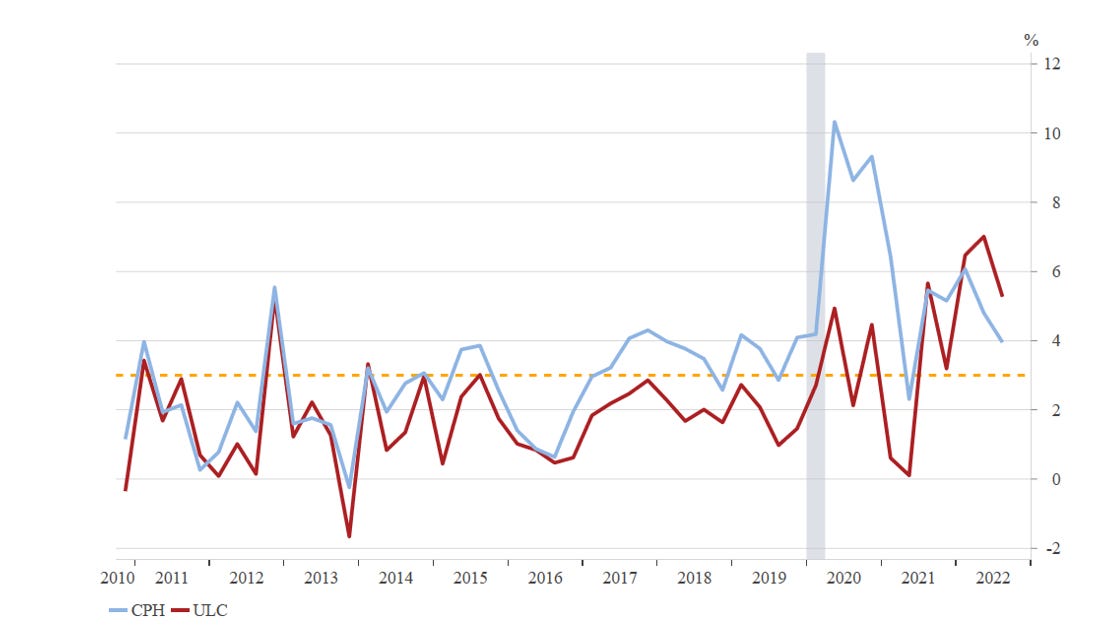

Compensation Per Hour (CPH) and the Unit Labor Cost (ULC) are from the “Productivity and Costs” report. The former (CPH) relates more to demand since it estimates the change in all worker compensation forms (wages and salaries, supplements, and employer contributions to employee benefit plans) net of taxes. The latter (UCL) relates more to employers’ cost pressures since it estimates labor productivity or real output per hour.

The growth in total compensation is now around its pre-Covid level while unit labor costs remain well above it, though both have moved down recently. These two are mixed; the former shows wage pressures easing, but the latter does not.

In closing.

We are skeptical that there are clear signs of wage disinflation, but we are also unsure that there are convincing signs of re-acceleration. The Fed staff likely agree.

Why? The Fed focuses on the highest-quality measures of wage growth tied closely to demand, which are the most likely to push up inflation. The Employer Cost Index (ECI) and Compensation per Hour (CPH) meet that criteria. Taken together, they are not showing clear signs of slowing yet.

The Fed staff update on Friday for Chair Powell went probably something like, “We don’t ‘trust’ the 0.6% monthly change in November. Underlying wage growth is likely lower, though the coming reports could prove us wrong.”

We agree the signs of wage growth slowing are limited. Plus, wage growth is often persistent; thus, we expect that it will take some time for it to slow. Finally, wage growth remains higher than pre-Covid when the Fed was at its 2% inflation target.

I want to thank Riccardo Trezzi for sharing his expertise on my Subtack today. Again, please consider subscribing to his paid-only newsletter. He publishes analysis of inflation data, related research, and comments from Fed officials.

Any thoughts on these wrt to your points about wages being impacted by (1) hours and (2) what about Oct/Sept revisions?

https://twitter.com/fcastofthemonth/status/1602340034807463936?s=46&t=M8t9tHHBh11f1lzIWqvmwQ

https://twitter.com/jasonfurman/status/1598819086003159040?s=46&t=M8t9tHHBh11f1lzIWqvmwQ

What if I were to show you how a single policy implemented at a strategic point in the economic process not only ended any possibility of inflation, but resulted in what is considered impossible in every economic orthodoxy, that is, BENEFICIAL price and asset DEFLATION.

First a little ground work. All monopolies are problematic. Why, because they fly in the face of Lord Acton's dictum that power corrupts and absolute power corrupts absolutely. So any time you break up a monopoly on whatever level you're solving a major problem. Secondly, we know from Steve Keen that the basic problem with the current macro-economic orthodoxy is they ignore "money, debt and banks". I would take that analysis a little higher by saying what is the current paradigm of new money and debt that is created only by banks/the banking system?

Think about it for a second, according to Keen's excellent calculus and research private debt will inevitably build up and destabilize an economy unless we run fiscal deficits. This is an historically verifiable systemic truth, but it doesn't recognize the core of that core economic problem, namely the

current (human civilization long) MONOPOLISTIC paradigm for the creation and distribution of new money. And that paradigm concept is...Debt as in burden to re-pay ONLY. The word ONLY marks it as a monopoly paradigm. In other words whether new money/credit was created by the Palace or by private banks it has ALWAYS been created ONLY as a debt that (allegedly) MUST be re-paid. That is the paradigm, the operant factor for the ENTIRE PATTERN of new money.

Historically, how do paradigm changes occur. 1) anomalies/problems build up around the current paradigm and we are deep into this process, 2) a new paradigm concept is floated and historically laughed at for longish periods of time, 3) a new tool and/or insight is discovered that enables the new paradigm concept (which concept by the way is always in complete opposition to the old/current paradigm making it apparently illogical and hence difficult for the scientific community to embrace it) 4) regardless, the application of the new concept resolves the old concepts major problems and in doing so brings virtually universal benefits while overturning orthodoxies that have grown up around it.

So what is the new monetary and financial paradigm and what benefits does its most strategically efficacious application bestow upon us? What is the opposite of burden to ALWAYS repay? Why Monetary Gifting of course, and specifically new paradigm concept is: Abundantly Direct and Reciprocal Monetary Gifting. And where and when is it implemented? At the universally participated in point in the entire economic process, namely retail sale. And what is the single policy that is the very expression of the new paradigm itself? A 50% Discount/Rebate policy at the point of retail sale.

What does this policy immediately, continuously, mathematically and temporally do? 1) it immediately doubles everyone's purchasing power so if you make $30k/yr. you can now potentially purchase $60k worth of goods and services with that $30k, 2) with the rebating back of the discount the merchant gives to the consumer it therefore potentially doubles the demand for every enterprise's goods and services and the "kicker" is 3) because a) every individual agent participates in retail sale and b) retail sale is the terminal summing point of all costs including profit for every item or service and c) also the terminal ending/exiting point of the entire economic process and d) hence by definition the terminal expression point for any and all significant economic factors, like for instance inflation...it not only ends any possibility of inflation it implements BENEFICIAL price and asset DEFLATION into profit-making economic systems. Holy orthodoxy and mind blowing inversion of reality is that!? But then that is what every paradigm change applied does to one degree or another. There are a lot more enabled benefits than this in the entire policy program of the new monetary paradigm in my book, on my substack and Patreon websites.