Powell Has Been Here Before

It’s three weeks into the war in Iran, and when the dust settles after today’s Fed meeting, the potential economic costs are likely to feel more real. The headlines will be hawkish, highlighting the Fed’s greater emphasis on inflation, but downside risks to employment and disposable income will also be heightened. Stagflation concerns are back.

Key points:

Be realistic. The economic consequences of the war in Iran could be substantial, and the Fed must plan for all contingencies. Even if their base case is only a temporary disruption, the uncertainty at this point is immense. Risk management will be a dominant theme.

Pay attention to the FOMC statement. It’s a consensus view. The Fed will hold rates in the range of 3‑1/2% to 3‑3/4%, as expected before the war began. The stagflationary impulses of the war warrant including “two-sided risks” in guidance on the policy rate, meaning the next move could be a hike or a cut. Previously, the committee had signaled that the next move would likely be a cut. The main theme will be patience in the service of collecting information, paired with a commitment to move as soon as direction is clear. There could be up to three dissents (Miran, Bowman, and Waller) in favor of a cut, but given how fluid the situation in the Middle East is, there ought to be full agreement to hold.

Ignore the Summary of Economic Projections (and the so-called dot plot). The Fed suspended the SEP in March 2020 due to the heightened uncertainty at the start of the pandemic. They should do the same in March 2026. The SEP is a set of baseline forecasts. We know too little about the war in Iran for this to be a useful exercise. Now would have been a great time for scenarios, as Ben Bernanke proposed. Setting aside my ‘what-they-should-do’ views, the Fed will publish the SEP in its usual format, and it will be hawkish.

Listen carefully to Powell. Risk management has been central to his leadership of the Fed, and the war in Iran is the latest supply shock under his tenure. The press conference is an opportunity to discuss risk scenarios. There are plausible events that could lead to a cut, extended pause, or hike this year. As he did in the pandemic, Powell will bring humanity. The war in Iran is more than prices at the pump or paychecks in the United States; the effect on people in the Middle East and around the world is real, and the objectives go far beyond the Fed’s dual mandate.

Don’t overinterpret a hawkish SEP.

The SEP is likely to be hawkish—higher expected inflation and fewer rate cuts. In December, the median Fed official expected one 25-basis point cut this year and another next year. The updated projections this month are likely to have a median of no cuts this year and one next year. The longer run rate might even be revised up.

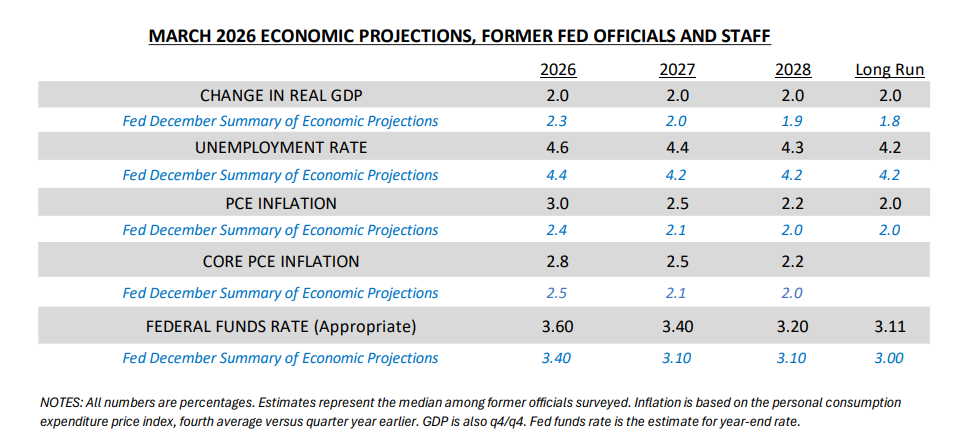

A good gauge is projections from a few dozen former Fed officials and former Fed staff organized by Jon Hilsenrath. (Hilsenrath is a former WSJ Fed journalist, and a very astute observer of the Fed in his own right.) The median projections from this group are below and are compared to the Fed’s SEP in December. The revisions to the median are downbeat: lower growth, higher unemployment, and higher inflation, though modest in magnitude, reflecting a temporary disruption from the war.

Even with a temporary disruption, the entire path of the federal funds rate from 2026 through the longer run is revised up. The median in this group of former Fed officials and staff, as with the median among current Fed officials, masks wide disagreements about appropriate monetary policy. The war in Iran has only amplified that disagreement.

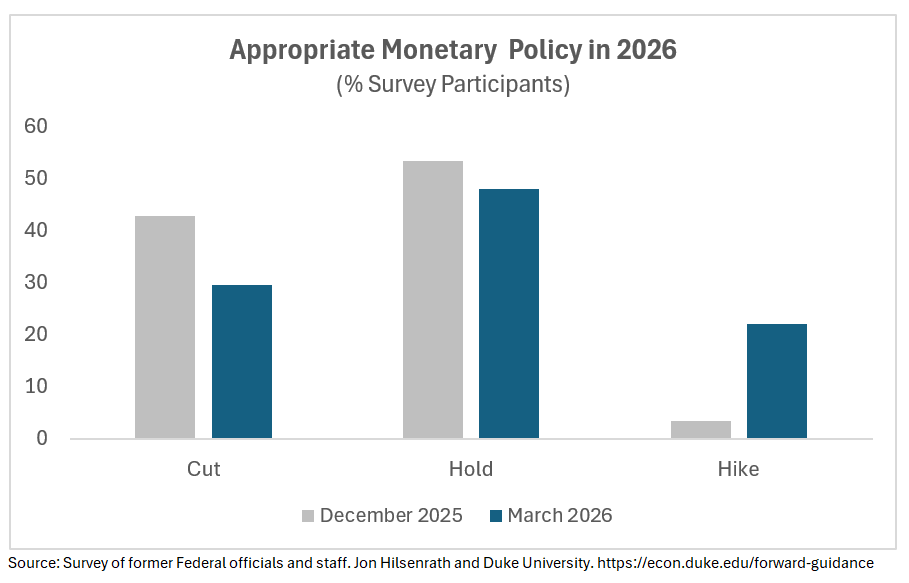

In the survey of former Fed officials and staff, the hawkish shift is clear. At the end of last year, less than 5% of participants thought a hike in interest rates would be appropriate in 2026; now, more than 20% see a hike as appropriate. The percent who view a cut in 2026 as appropriate dropped from 40% to 30% across the two surveys.

I expect a similar hawkish shift in the actual SEP. Keep in mind that the SEP is a communication device, and some Fed officials will see a benefit in erring on the side of hawkish communications to bolster the Fed’s credibility as an inflation fighter. The SEP is too blunt a tool for delivering such a nuanced message, and the uncertainty about the war is immense, so I would caution against reading too much into the SEP as a prediction of likely monetary policy this year.

Powell's supply shock playbook.

In terms of how the Fed should respond, the war in Iran calls up comparisons to oil embargoes of the 1970s or Russia’s invasion of Ukraine in 2022. That’s too narrow a scope. The effective closure of the Strait of Hormuz is a major global supply shock, raising the cost of energy and related products. The pandemic, which snarled global supply chains and restricted the labor force, was a supply shock. Tariffs—in the first and second Trump administrations—which raise the cost of imported goods and reduce productive efficiency, are also a supply shock.

Put simply, Powell’s tenure as Fed Chair since 2018 has been navigating one supply shock after another. The key questions for the Fed now are familiar: how long will the supply disruption last, how severe will it be, and whether it will become embedded in inflation expectations. Also, the high degree of uncertainty, especially at the onset, is familiar. Finally, as with last year, and markedly different from 2022, the supply shock from the war in Iran coincides with a labor market with some weakness. Once again, there are upside risks to inflation and downside risks to employment.

At the press conference, I expect Powell to elevate the risk-management approach and to reiterate how the Fed operates when both sides of the dual mandate are at risk. The Fed’s strategic framework lays out the approach:

The Committee’s employment and inflation objectives are generally complementary. However, if the Committee judges that the objectives are not complementary, it adopts a balanced approach to promoting them, taking into account the extent of departures from its goals and the potentially different time horizons over which employment and inflation are projected to return to levels consistent with its mandate. The Committee recognizes that employment may at times exceed real-time assessments of maximum employment without necessarily posing risks to price stability.

Put simply, when there’s tension between employment and inflation, the Fed tries to address what it sees as the biggest, most persistent problem. It’s trying to avoid the worst outcome.

The Fed’s three rate cuts last year fit this approach. Fed officials viewed the downside risks to employment as a more urgent concern than the upside risks to inflation. The SEP, which focuses on baseline forecasts rather than risk scenarios, is poorly designed to capture these trade-offs.

However, relative to before the war in Iran, I expect Powell to sound more hawkish today. The upside risks to inflation are worse than with the tariffs last year. A reasonably bad risk last year was that inflation would become stuck at 3%. If the war in Iran were protracted, it could cause a surge in inflation. It’s not to say that’s likely, but at this point it cannot be ruled out. On the flip side, a recession cannot be ruled out either. Incoming data chipped away at signs of improvement in the labor market. It’s a balancing act in a moment of great uncertainty.

In an interview a few weeks ago, Fed Governor Chris Waller was asked to assess developments in the Middle East. He emphasized scenarios:

What you’re gonna see is a spike in gasoline prices. Thinking about policy going forward, it’s unlikely to cause sustained inflation. That’s one reason we don’t look at energy prices. That’s why we look at the core. It’s a better predictor of future inflation. Once the supply chain issues unravel, the prices will come back down. It becomes bigger if it becomes more permanent. Then it will bleed into other parts of the economy. In the 1970s, the oil shocks kept coming and coming. This is more like a one-off event.

Until the worst-case scenarios of a more persistent supply shock are off the table, the Fed is likely to tread cautiously and hold rates steady.

In closing.

Today’s Fed meeting is likely to be a reality check. The situation in the Middle East is serious, and the risks to the US economy are substantially greater than they were even a month ago. The concerns about inflation and the potential for the Fed’s next move to be a rate hike may draw the most attention, but the key takeaway should be a focus on risk assessment and risk management. It’s a difficult time, but it is one for which the Fed has prepared.

Sahm points out something important that the Fed has been navigating supply shock after supply shock with the same blunt tool. But that raises a harder question. If rate hikes can't fix broken supply chains or oil embargoes, and the cost is always borne by workers through unemployment and tighter credit, why is Congress still not part of this conversation? The Fed gets called in because fiscal policy won't show up, not because monetary policy is the right answer.

Love and value your insight, as ALWAYS, Claudia. I read every word. Your point about Powell adding humanity into the policy management equation is spot on.

EMPATHY - an emotion totally lacking in this regime.

https://www.youtube.com/watch?v=dQHUAJTZqF0&list=RDdQHUAJTZqF0&start_radio=1