It's time for the 'dot plot' to go.

Tomorrow we learn when each Fed official thinks it will be the right time to raise interest rates. So, is it liftoff in 2022 vs 2023? Pointless to guess, even harmful. Solution: Fed, stop guessing.

Tomorrow the Federal Open Market Committee will announce its latest decision on how much to support the economic recovery. Some will be watching closely, including analysts and traders on Wall Street; wealthy investors; Fed journalists; and a small group like me who simply LOVE the Fed. Chances are you won’t watch. I don’t blame you. The Fed doesn’t talk to you. It should.

I have A LOT to say. One snippet from my TV interview on Bloomberg yesterday:

“I frankly don’t care what Jim Bullard [Federal Reserve Bank President of St. Louis] thinks is appropriate monetary policy is … ”

It’s not personal. I’m not angry at Jim. He’s doing his job within a broken system. Robert Kaplan at Dallas and Eric Rosengren at Boston — two other Fed officials —are another matter. They should resign for actively trading during the past year. (Thanks to Michael Derby for breaking the infuriating story.)

The Federal Reserve is a one of the most powerful government institutions in the United States and one of the least understood. It’s time the Fed got serious about solving that problem. It’s their fault. The Fed’s words and its tools are confusing. The worst offender? The infamous ‘dot plot.’ No, the Fed does not use matrix printer, though the solution is the same. Throw it away and get with the times.

Do not connect the dots

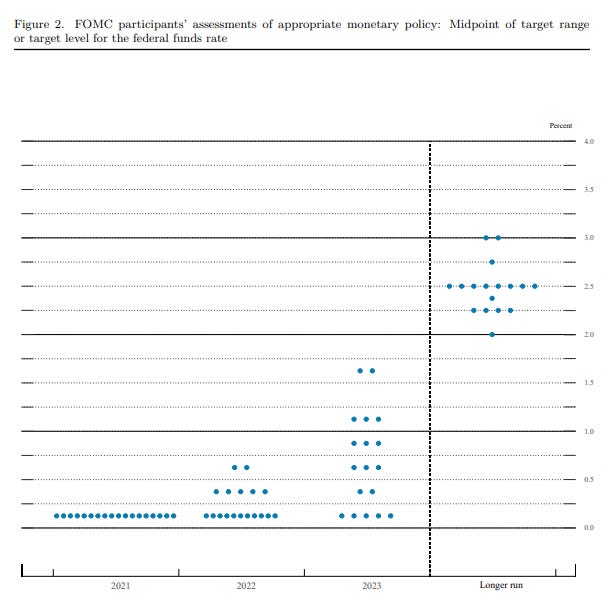

Here is the Fed’s latest dot plot from June.

How could such a boring chart that looks like the Space Invaders game from the late 1970s get me so riled up and cause financial markets to move? Each dot is a Fed official’s guess of where they think the Fed’s interest rate should be over the coming years. As the economy recovers, the Fed should gradually reduce its support.

The big debate is when. No one knows but Fed officials are happy to guess. What are these dots exactly? Here’s the Fed’s clear-as-mud explanation:

“Each shaded circle indicates the value (rounded to the nearest 1/8 percentage point) of an individual participant’s judgment of the midpoint of the appropriate target range for the federal funds rate or the appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run. One participant did not submit longer-run projections for the federal funds rate.”

(Guess who’s missing their dot. Come on, Jim, play along or delete all yours.)

I worked at the Fed for over a decade. I was there when the dots were born in October 2007. I understand why then-Chair Ben Bernanke thought they would help clarify the Fed’s thinking for the public. He’s a macroeconomist’s macroeconomist. I’m a macroeconomist too, albeit less popular among the tribe. I get it, AND I firmly disagree. Those dots are NOT the way to speak more clearly. They are confusion.

Fast forward to 2021. (No, inflation hawks it is NOT 1971.) The Federal Reserve is pursuing its new strategy. As Heather Long reported. it is a strategy to avoid the Fed’s mistaken decision to raise rates too soon. Why? They made bad forecasts.

Ain’t got no crystal ball

Year after year, the Fed expected inflation to settle persistently at their target of 2% in the next few years. Guess what? It did not.

Imagine if at your annual review—one that didn’t look so hot—you promised your boss that next year you’d get your job done well. Then next year rolls around, and it’s same old same old. No raise for you. You might eventually be put on a performance improvement plan. The Fed was. It took a while, but the Fed finally admitted it should STOP USING ITS FORECASTS TO DRIVE POLICY DECISIONS.

What was the cost of their past mistakes? After the Great Recession, raising interest rates too soon delayed the recovery and people getting back to work. AND it meant they consistently fell short of 2% inflation target. So much for the dual mandate. So much for a job well done. Do better, Fed.

Hey, let’s try something new

Hope springs eternal and every day is a new day. The Fed thought hard about how to not repeat its past mistakes. The result was a new framework, with an “average” inflation target of 2% and a goal of “inclusive” and “broad-based” employment.

As I wrote earlier, it is a BIG change and it’s a robust one:

The Fed needed the push. It got it. A fun fact about Fed culture. Pushing for change is like moving a mountain. Frankly, [metaphorical] earthquakes and volcanic eruptions—my specialty—are necessary. And then when the Fed finally moves, always after years and years of deliberations, IT DOES NOT MOVE BACK. It took me a while as a junior staffer to figure this out. Patience, perseverance, and rock solid arguments do pay off at the Fed.

The FOMC voted unanimously for its new framework—one grounded in actual inflation and jobs, not their broken crystal-balls. It’s time to live it. Ditch the dots.

Wrapping Up

The dot plot was born in a world where the Fed’s decisions relied heavily on its forecasts. That world is gone. Reality is in; forecasting is out. It’s time for the dots to go. Watch Chair Jay Powell tomorrow at the press conference. See how many times he tries to draw attention away the dots. DO NOT make it into a drinking game. Even with coffee, don’t do it. You’ll be up on all night. If Jim Bullard or Richard Kaplan or any of those Reserve Bank Presidents set off a taper tantrum with their dots, I will totally lose it. Ignore the dots.

Say after me, “A good Fed is a boring Fed.”

Programming Note: Soon some of my deeper dive posts on the Fed will be for paid subscribers only. Please consider supporting my Substack. You will get you extra insights. See details here. And you will help me write regularly here for everyone on economics, including on the Fed.

FOMC Members go around blindfolded!

https://thefaintofheart.wordpress.com/2015/10/25/looking-for-wally-when-there-are-many-wallies/

To have the helmsperson predict where they expect to set the rudder some time in the future is silly. It will be set (or ought to be) at the point that will have the vessel on course given the wins and currents AT THAT TIME. More useful would be to have each member disclose their opinion of what the value of some instrument should be right now ad possibly what it should have been in the past