Can the Fed bring inflation down alone?

No, it cannot.

Here’s my opinion piece in the Financial Times on the limits of monetary policy:

My post is a talk I am giving at Gettysburg College on the same topic.

The Fed’s tools don’t work well on supply-driven inflation.

Key takeaways:

The Fed’s interest rate tools are best suited for demand-driven inflation.

Covid and the war in Ukraine caused supply-driven inflation.

Financial markets pass along the Fed’s rate but don’t always agree.

Household finances are good, so interest rates are affecting demand less.

It’s best to solve labor shortages with more workers than fewer customers.

Congress and the White House have tools to solve supply-driven inflation.

A key lesson from the past three years is that disruptions to supply can occur rapidly and recover slowly. The pandemic and war in Europe created substantial inflationary pressure, including on food, energy, and housing, which the Fed can’t fight well.

The Fed’s tools are imprecise and depend on others.

Fed rate hikes are transmitted through financial markets. But the federal funds rate is just one factor affecting the market interest rates at which households and businesses borrow and save, so market interest rates are just one factor affecting demand.

Financial markets had disagreed with the Fed on what future policy will likely be. Since the fall, markets disagreed even as the Fed raised rates and said it would keep them high. So, market conditions became less restrictive, making policy less effective.

So how’s it going for the Fed?

The Fed’s 4.75 percentage point hike has affected interest rate-sensitive sectors like housing. Mortgage rates reached 7%; housing starts and home sales plummeted. Even so, employment in this sector has held up so far, limiting the broader feedback.

The Fed is struggling to slow down consumer spending. Strong demand limits the incentive for businesses to raise prices less or cut them. It also keeps the labor market strong. Interest rates are struggling to break that dynamic.

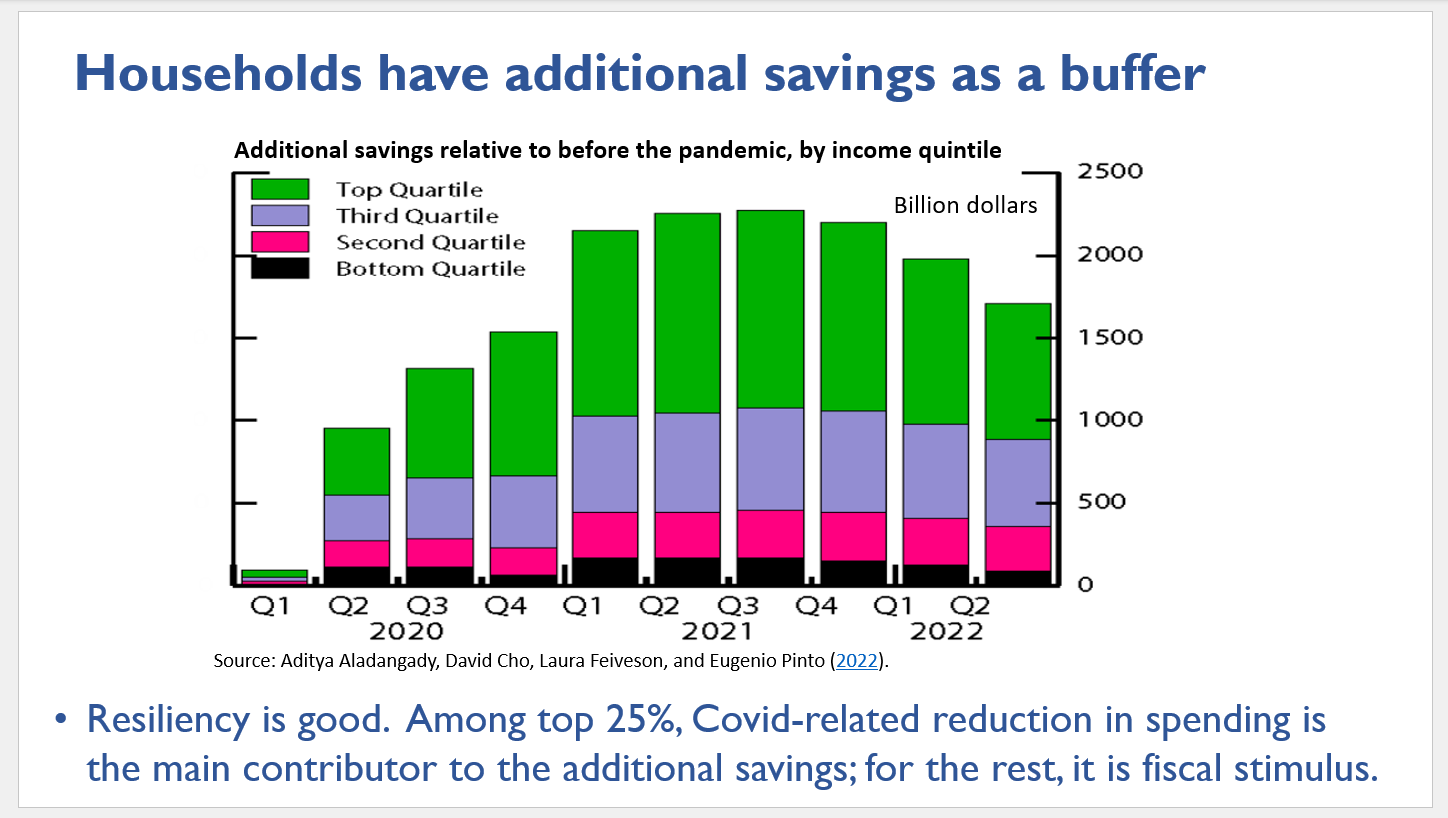

Why is the consumer doing well despite high inflation?

Households exited the recession with more savings, not less. Shutting down the economy meant many households spent less, especially on services. Fiscal relief also added to savings. The extra savings helps support demand now.

The bright shining spot is the strong and inclusive labor market recovery. Unemployment is very low, and wage growth remains above pre-Covid levels. Paychecks are an important source of income. And income supports spending.

Fiscal policy can address supply-driven inflation.

The population grew more than expected last year, owing mainly to immigration. Julia Coronado argues that while immigrants add to demand, their high labor force participation rate will help ease labor shortages. The Fed doesn’t control immigration.

Gas prices are an example of fiscal policy addressing supply-driven inflation. When the war in Ukraine began, energy prices skyrocketed. The White House opened the strategic reserve to add oil to global markets and encouraged domestic production.

Congress enacted three major pieces of legislation to make our economy more resilient. Some of the measures will protect against future inflation.

Another key advantage of fiscal policy is that it is more targeted and direct. Some industries are systemically important for inflation in their sector and others.

In closing.

All policymakers must work to make our economy more resilient. Learn the lessons.

I'll share this on Twitter later on, this is another solid piece here. With regards to fiscal policy, yes congress is going to have to do more (with a divided congress likely won't happen) but two things we can talk about that will help are the Federal Job Guarantee and also the Green New Deal. Botton line, indeed the federal reserve alone is doing its best to start a recession and that's just plain wrong.

Awesome read. The right tool for the job is important. I have broken many a screwdriver using it to hammer nails.